Trick Aspects to Think About When Obtaining an Equity Finance

When considering making an application for an equity finance, it is important to browse via different crucial factors that can substantially influence your monetary well-being - Equity Loan. Comprehending the kinds of equity car loans available, assessing your qualification based upon economic factors, and meticulously taking a look at the loan-to-value proportion are vital initial actions. However, the complexity strengthens as you look into contrasting passion prices, charges, and repayment terms. Each of these factors plays an important function in figuring out the general price and expediency of an equity financing. By carefully scrutinizing these elements, you can make informed decisions that line up with your long-term economic goals.

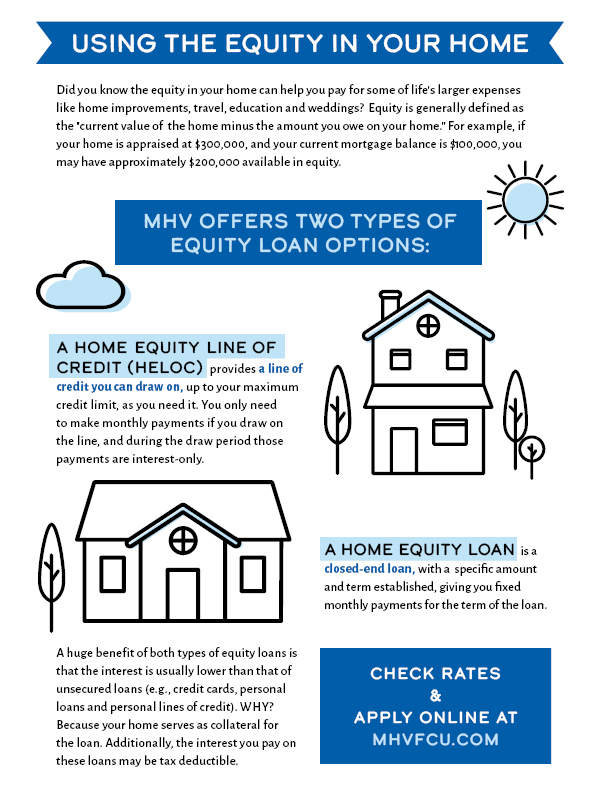

Kinds Of Equity Financings

Numerous monetary institutions offer a range of equity financings customized to satisfy diverse loaning needs. One usual type is the standard home equity finance, where house owners can borrow a round figure at a set rate of interest rate, using their home as collateral. This sort of financing is perfect for those who need a large amount of cash upfront for a certain purpose, such as home renovations or debt loan consolidation.

Another popular option is the home equity line of credit rating (HELOC), which works more like a bank card with a rotating credit report restriction based on the equity in the home. Debtors can attract funds as needed, approximately a specific restriction, and just pay interest on the amount made use of. Home Equity Loan. HELOCs appropriate for continuous costs or projects with unpredictable prices

Additionally, there are cash-out refinances, where property owners can re-finance their existing mortgage for a higher amount than what they owe and obtain the distinction in cash - Alpine Credits Equity Loans. This kind of equity car loan is valuable for those wanting to make the most of reduced passion prices or accessibility a big amount of cash without an added month-to-month settlement

Equity Funding Eligibility Variables

When considering eligibility for an equity car loan, monetary establishments commonly examine variables such as the candidate's credit rating, income stability, and existing financial obligation commitments. A vital aspect is the credit rating, as it reflects the debtor's creditworthiness and capability to pay off the financing. Lenders prefer a greater credit history score, normally above 620, to minimize the danger connected with financing. Earnings stability is another vital aspect, demonstrating the borrower's capability to make regular car loan settlements. Lenders may require evidence of regular revenue with pay stubs or income tax return. Additionally, existing debt obligations play a considerable function in determining qualification. Lenders assess the borrower's debt-to-income ratio, with lower proportions being extra beneficial. This proportion shows just how much of the customer's income goes in the direction of paying off financial debts, affecting the lending institution's choice on car loan approval. By thoroughly evaluating these elements, banks can determine the applicant's qualification for an equity car loan and establish suitable lending terms.

Loan-to-Value Proportion Considerations

A reduced LTV proportion indicates less threat for the loan provider, as the consumer has even more equity in the home. Lenders normally prefer reduced LTV ratios, as they offer a greater pillow in situation the consumer defaults on the lending. A higher LTV ratio, on the other hand, recommends a riskier financial investment for the loan provider, as the consumer has much less equity in the building. This might cause the loan provider enforcing higher rates of interest or more stringent terms on the lending to mitigate the boosted risk. Borrowers ought to intend to maintain their LTV ratio as low as feasible to enhance their possibilities of authorization and protect extra favorable lending terms.

Rate Of Interest and Charges Comparison

Upon examining rate more tips here of interest and charges, consumers can make enlightened choices pertaining to equity lendings. When contrasting equity loan alternatives, it is vital to pay attention to the rates of interest used by different lending institutions. Rate of interest can dramatically impact the total expense of the finance, influencing month-to-month settlements and the overall quantity repaid over the car loan term. Lower rate of interest can cause considerable savings with time, making it critical for customers to search for the most competitive prices.

Besides rate of interest, debtors should also think about the different charges related to equity fundings - Alpine Credits Home Equity Loans. These charges can consist of source costs, assessment fees, shutting prices, and prepayment charges. Source fees are charged by the loan provider for processing the financing, while assessment fees cover the cost of examining the property's value. Closing prices incorporate various fees connected to finalizing the lending contract. Prepayment penalties might apply if the customer pays off the lending early.

Payment Terms Assessment

Reliable evaluation of repayment terms is critical for consumers seeking an equity loan as it straight affects the funding's price and economic outcomes. When analyzing payment terms, customers ought to thoroughly examine the lending's duration, regular monthly settlements, and any potential charges for early repayment. The finance term describes the size of time over which the debtor is expected to settle the equity loan. Shorter car loan terms typically cause greater monthly repayments but lower general passion expenses, while longer terms offer lower month-to-month repayments however may cause paying even more rate of interest in time. Borrowers need to consider their financial circumstance and objectives to identify the most ideal payment term for their demands. In addition, understanding any kind of fines for early repayment is crucial, as it can affect the versatility and cost-effectiveness of the financing. By thoroughly evaluating settlement terms, debtors can make educated decisions that straighten with their financial goals and make certain effective funding monitoring.

Verdict

To conclude, when looking for an equity lending, it is very important to consider the kind of funding offered, qualification variables, loan-to-value ratio, rate of interest and fees, and repayment terms - Alpine Credits Home Equity Loans. By meticulously reviewing these vital factors, borrowers can make informed choices that align with their monetary objectives and conditions. When looking for an equity financing., it is crucial to thoroughly study and compare alternatives to guarantee the finest feasible end result.

By thoroughly evaluating these factors, economic establishments can establish the applicant's eligibility for an equity financing and establish suitable loan terms. - Home Equity Loan

Rate of interest rates can considerably affect the total expense of the financing, impacting regular monthly payments and the complete amount repaid over the finance term.Reliable assessment of repayment terms is essential for consumers seeking an equity lending as it straight affects the finance's cost and financial end results. The car loan term refers to the size of time over which the consumer is expected to repay the equity funding.In conclusion, when using for an equity funding, it is essential to take into consideration the kind of car loan readily available, eligibility aspects, loan-to-value proportion, interest prices and costs, and repayment terms.